“I want tax-free investments and a tax-free retirement.”

That is the response I hear over and over again when I speak with investors about what they want from their investments. In fact, questions about taxes and the tax-advantaged nature of real estate investing are easily the biggest subjects I address in these conversations.

As often as the subject comes up, you’d think people were obsessed. Who could blame them? After all, most high-net-worth, high-income investors get crushed with taxes. Every year around April, they shudder in fear knowing there will be countless hours of sifting through receipts. And their reward is a grotesquely demoralizing high tax bill.

Thus their mantra, “I want tax-free investments and a tax-free retirement.”

The History of This Misery

We have the 16th Amendment to thank for this painful annual ritual. It gave Congress the right to levy an income tax, which they quickly utilized by enacting the Revenue Act of 1913. That law spanned 400 pages and set a top tax rate of 7%.

It started primarily as a tax on the rich as the first $3,000 of income was exempt. After that, the bottom tax rate of 1% applied to those making between $3,000 and $19,999 ($72,000 to $480,000 in today’s dollars).

Today, the sheer size and complexity of the tax code is mind-boggling. The rate structure can lead some to feel like they are subject to confiscation more than taxation. That same $480,000 in income that was taxed at 1% in 1913 had a top marginal tax rate of 39.6% in 2016.

Our Biggest Expense

It is incredibly hard to get ahead today, let alone save for tomorrow when you shoulder that kind of tax burden. Make no mistake; the average accredited investor’s biggest expense is taxes.

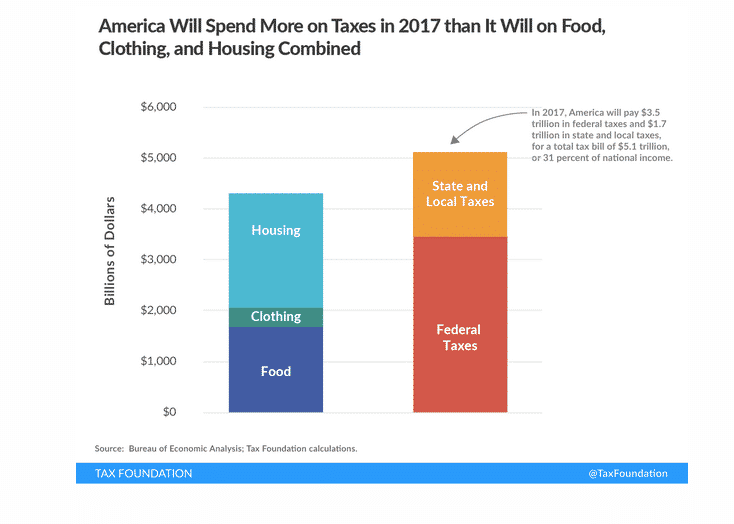

The Tax Foundation has looked at the subject and found that between state, federal, and local taxes, we as a nation, pay approximately $5 trillion in taxes a year. That is more than we pay for our basic needs.

Is it any wonder why people want tax-free investments and a tax-free retirement?

Tax-Free Investments and a Tax-Free Retirement

When you say the words tax-free investments, most people think of municipal bonds. But in today’s low-yield environment, good luck getting ahead financially by investing in municipal bonds. Yeah, you can get your tax-free investment, but you might as well forget about that tax-free retirement because you’ll never be able to retire with returns that low.

So let’s get real…returns matter!

And for those of us who want better than reasonable returns, the taxman is lying in wait ready to pounce. You are either going to give him your pound of flesh or you are quickly going to get comfortable with the subject of tax deferral.

Tax Deferral

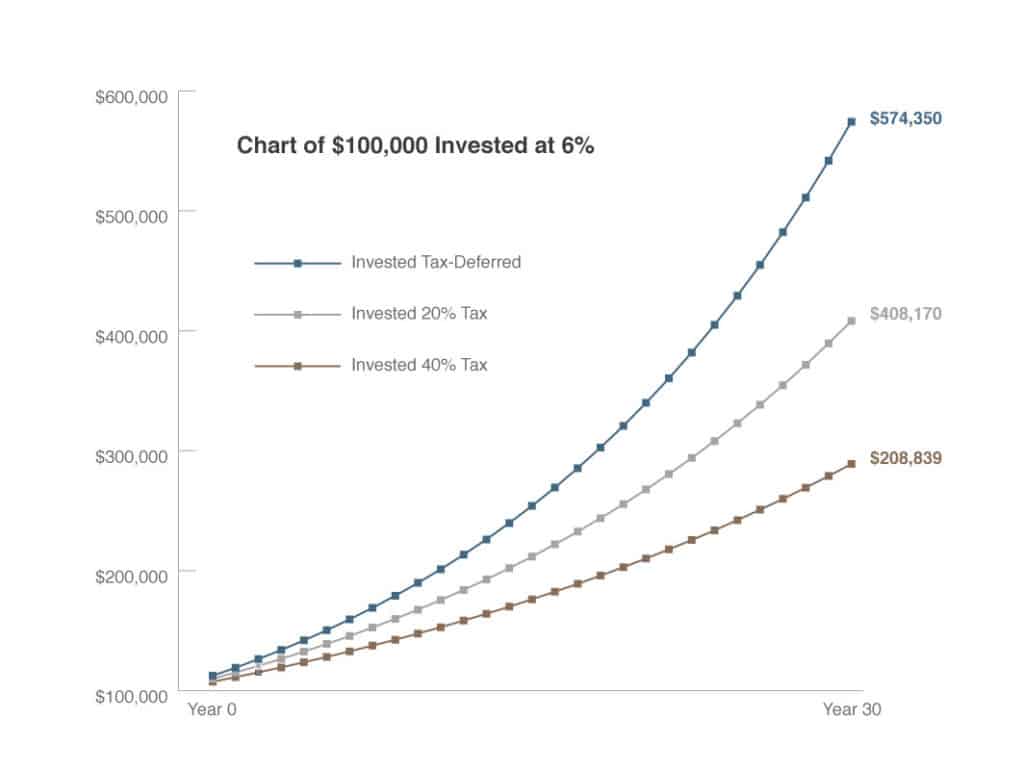

Investopedia defines tax deferral as investment earnings that accumulate tax-free until they are taken. To better understand the significant value of tax deferral, consider the graph below.

This graph shows three identical investments of $100,000 that achieve a steady 6% return per year. One of the investments is taxed at 40% per year, another at 20%, and the final one is tax-deferred. As you can see, over a 30-year period, the tax-deferred account accumulates significantly more wealth than the taxed accounts.

Tax deferral = more money = higher compounding effect = greater wealth = better retirement

In fact, tax deferral is so important to creating retirement wealth that the government created tax-deferred retirement accounts for workers. Those plans go by various designations but include 401(k), 403(b), and IRA’s (just to name a few). These accounts come with various government rules such as not being able to withdraw funds until reaching the minimum age of 59 1/2 (with some exceptions). It is absolutely possible to own real estate in a qualified retirement plan.

Real Estate is Highly Tax-Advantaged

One of the many benefits of investing in apartments is the tax advantages. The cornerstone of those tax benefits is called depreciation.

Depreciation is a tax deduction that owners of property get to take annually until the entire asset has been completely depreciated. For resident occupied real estate, that time frame is 27.5 years. For non-resident occupied real estate (industrial, retail, office, etc.) the depreciation schedule is 39 years.

The logic behind depreciation allowance in the tax code revolves around the concept of useful life. To better understand this concept, let’s look at the depreciation schedule for new computers purchased by a business. In this example, the IRS allows businesses to depreciate their computers over a five-year period.

In the scenario of computers, useful life closely approximates actual life. Fortunately for apartment investors, useful life (27.5 years) is nowhere close to their actual lifespan. If it was, then every house and apartment complex built-in or before 1990 would be worthless; and we all know that isn’t true. So while our properties are actually appreciating in value, the IRS allows us to depreciate them. This paper loss or a phantom loss creates incredible value in the form of tax-deferred income.

Calculating Depreciation

Once you understand that depreciation can allow you to create years and years of tax-deferred income it is easy to understand why so many people invest in real estate. But how is depreciation calculated?

The first step is to separate the value of the property into the improvement (physical structure) and the land. It’s important to remember that land is not depreciable. So a $10 million property might have a land value of $2 million. That leaves the value of the improvement at $8 million. In this scenario, the annual depreciation would be:

Depreciation = $8 million / 27.5 years

Which is equivalent to $290,909 a year in paper losses over the next 27.5 years. Depreciation is what allows our average investor not to pay any tax on the income they earn from us for the first 10 – 13 years. And for those who want to defer those taxes even longer, they simply just buy more real estate. Because depreciation schedules can be combined, it is possible to defer taxes on investment income for decades.

Start Investing in Commercial Real Estate for a Tax-Free Retirement

So the next time you hear someone say that they want tax-free investments and a tax-free retirement just know that you are speaking to someone that understands the real drag on wealth accumulation that occurs from taxes. These are people who likely would benefit from learning how to invest in commercial real estate. Having the potential to create stable streams of passive income coupled with equity growth all wrapped inside of a highly tax-advantaged framework makes investing in apartments hard to beat.