Yield or income investing is a critical component of my investment plan. Real estate investors call it cash flow. We know that if we create enough stable passive income streams, we become financially free.

With that said, growth is also a key component of my plan.

Yet some investors consider yield and growth an either-or proposition. The good news is that these two strategies aren’t mutually exclusive. You can have your cake and eat it, too.

First, let’s discuss each of these investment strategies.

Growth Investing

Growth investing primarily focuses on investments that provide capital appreciation or capital gains. It’s a search for up-and-coming investments believed to have the potential to increase in value over time.

In the stock market world, growth investing tends to be on the riskier side. Small-cap stocks, emerging market funds, and Internet and technology startups are examples of growth investments.

Growth investing tends to be an offensive strategy that is often recommended during the investor’s youth. As the investor nears retirement, switching to a more defensive strategy emphasizing capital preservation is common. It’s all about portfolio allocation. Over time, these portfolios drift away from growth investments and toward safer income investments.

Income Investing or Yield

Income investing is a strategy of purchasing assets that produce recurrent income. That yield can be in the form of interest, dividends, or distributions.

By owning assets that generate consistent income, these investors become less dependent on earned income. If they create enough recurrent passive income to cover their expenses, they can stop working for a paycheck if they choose to.

Yield can be found in savings accounts, money market funds, CDs, bonds, dividend stocks, and real estate.

Both yield and growth are components of overall total return.

Total Return Factors in Both Yield and Growth

The equation for total return factors in an investment’s growth and yield is expressed annually.

Total Return = (Growth + Yield) / Initial Investment

So, a $100,000 initial investment that grew in value to $105,000 over the last year while spinning off $5,000 in yield would have a 10% overall total return.

($5,000 in growth + $5,000 in yield) / $100,000 initial investment = 10%

It’s easy to see how income and growth investing are valuable. Unfortunately, yields are at or near historic lows and have been that way for several years.

Low Yield Environment

As valuable as income investing is, the yield has been drying up. Let’s look at some examples.

Savings Accounts

In July 2017, GOBankingRates.com reported that the average annual yield for savings accounts is a meager 0.06%. Unfortunately, many of the larger banks only pay 0.01%.

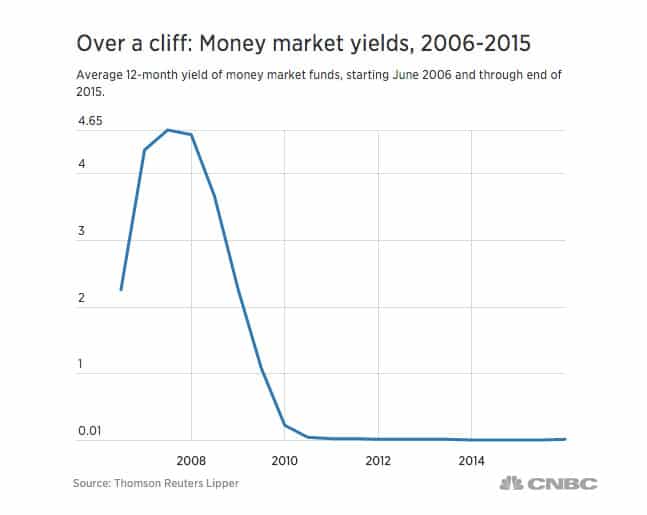

Money Market Funds

In 2007, money market funds’ average return was around 4.5%, but it has drastically declined over the last decade. In 2016, CNBC published the graph below and reported that the average return for money market funds was only 0.1%.

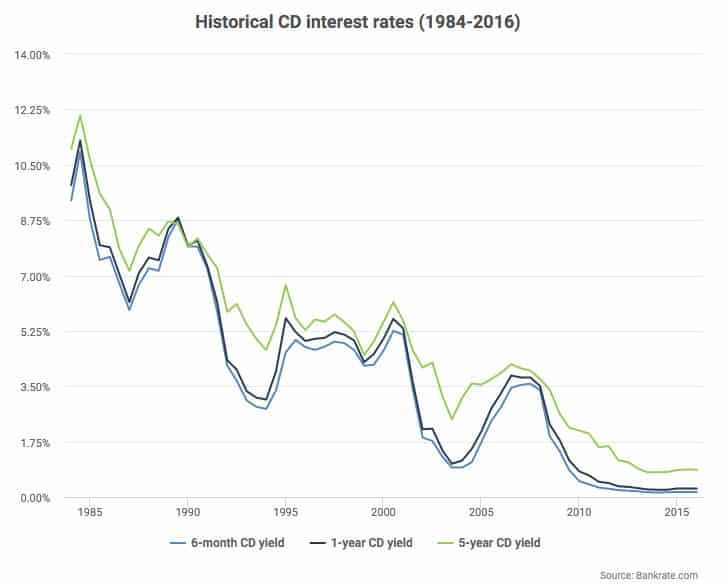

Certificates of Deposit (CDs)

Last year, Bankrate.com published data on historic CD interest rates from 1984 to 2016. The results, shown below, showed a disturbing trend in declining CD yields.

Bonds

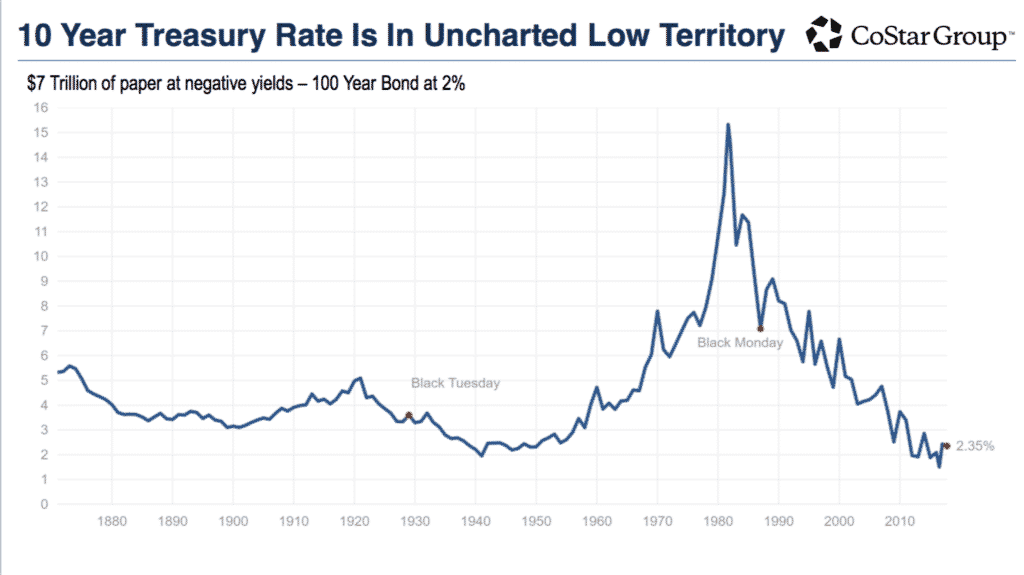

Government bonds have historically produced better yields than savings accounts, mutual funds, and CDs. While this remains true, bonds are also low compared to their long-term average. Currently, the annual yield on the US 10-year Treasury bond is just slightly better than 2%. Shorter-term government bonds are yielding less than 2% per year.

Dividend Stocks

While the S&P 500 dividend yield has historically been over 4%, investors haven’t seen those yields in decades.

Chasing Yield

Chasing Yield

With yields topping out at or around 2% and often much lower, it is easy to see why many investors are searching for better yields. But are they incurring more risk?

Unfortunately, as a rule, higher yield investing means higher risk. That is why so many financial advisors shun yield-chasing. They know that the increased risk often doesn’t justify the returns, and in the worst-case scenario, it may equate to little more than gambling.

Whether it’s high-yield junk bonds, hard money lending, individual dividend stock picking, or some other risky form of investing, chasing yield rarely makes sense.

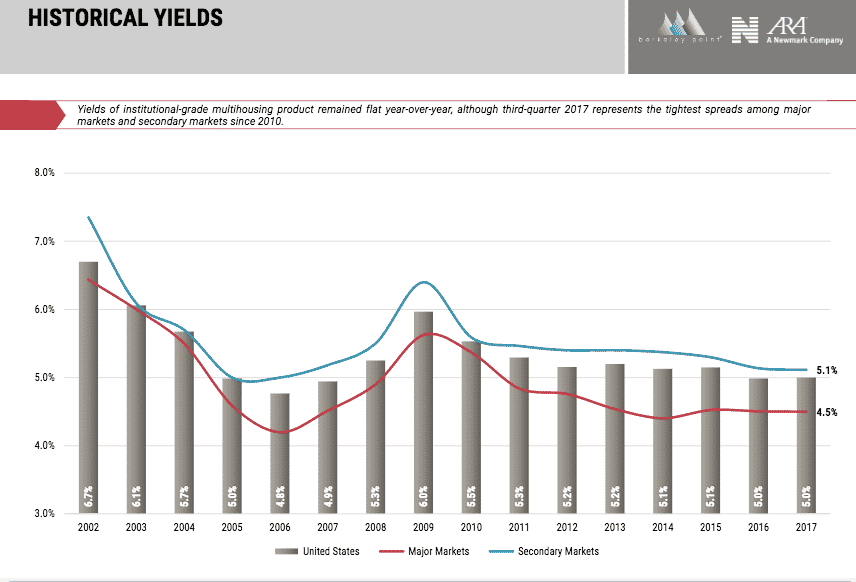

This is especially true when you understand that commercial multifamily real estate has a long track record of providing higher yields at a lower risk profile.

Commercial Multifamily Real Estate Breaks The Rules

You read that correctly; commercial real estate, in general, and multifamily, more specifically, has a long history of providing stock-like returns with lower bond-like risk. It’s the exception to the rule. It can provide two to four times better yields than the average dividend stock or government bond while maintaining a risk profile three to four times lower than the stock market.

It has had the best risk-adjusted return over the last 20 years by providing enhanced returns and lower volatility. That is why portfolios that added commercial multifamily real estate over the previous 20 years tended to do better than those made up of only stocks and bonds.

With that kind of history, why would anyone chase yield?

J.P. Morgan Asset Advisors said it best in their report, “Real estate: Alternative no more,” when they said the following:

“Is the current market environment heralding the realization of a new normal, a new world of uncertainty, heightened volatility, and slower growth? Perhaps, but the reality is that the investment portfolios focused on the “Big Two Traditionals,” bonds and equities (stocks), are forcing investors to compromise – either by sacrificing return for lower volatility or enhancing return at the expense of higher risk.

Real estate may offer a way out. This is why we believe real estate is increasingly being viewed, not as an alternative, but as an essential portfolio component.”

I couldn’t agree more. Have you added this essential component to your portfolio? If not, what are you waiting for?