The tax benefits of real estate investing make it one of the most attractive places to park your money, even during a recession. Individually, these tax benefits are powerful tools that dramatically increase the value of real estate investing. Collectively, they make apartment investing a home run. They are:

- Depreciation

- 1031 Exchanges

- Refinances

- Legacy Transfer/Beneficiary Deed

These real estate tax benefits are explained in detail below.

How Important Are the Tax Benefits of Real Estate Investing?

The greatest expense that many Americans face is taxes, which makes the subject of tax-advantaged investments so critically important.

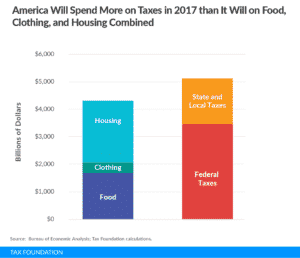

In fact, the Tax Foundation estimates that in 2017, Americans will pay $3.5 trillion in federal taxes and $1.6 trillion in state and local taxes for a total tax burden of $5.1 trillion. That is 31% of the nation’s income. Therefore, Americans will spend more on taxes than they will on their basic needs (food, clothing, and shelter).

Given the progressive nature of our tax system, high-income and high-net-worth individuals like our investors typically shoulder a much heavier tax load than the average American.

Therefore, it should come as no surprise that they are looking for highly tax-efficient investments. Many have heard about the tax benefits of real estate and they want to learn more.

In fact, one of the most common questions I get from investors is about taxes. Now I always preface these conversations with the disclosure that I am not a CPA or a tax attorney and that they should always seek advice from their trusted tax professional as to whether or not a particular tax strategy will work for their individual situation.

Having said that, I’m not a novice either. In my years working and investing in the multifamily apartment world, I’ve had the opportunity to see what really works.

Multifamily real estate carries some of the strongest tax benefits out there, and the cornerstone of those advantages is depreciation.

Depreciation – The Cornerstone Tax Benefit of Real Estate Investing

Rental property depreciation is an accounting convention that allows investors to write off the value of a property over time. For resident-occupied real estate, that time period is 27.5 years.

As an example, let’s look at a multifamily property valued at $34,500,000. Keep in mind that apartments have both a land value and a building value. Since land is not depreciable, its value would have to be subtracted out of the total. For the purpose of this example, let’s say that the land is worth $7,000,000. That would leave the value of the building(s) at $27,500,000. Again, that building value is what gets depreciated over 27.5 years. The formula looks like this:

$27,500,000 / 27.5 years = $1,000,000 a year in annual depreciation for the next 27.5 years.

That million dollars of annual depreciation represents a paper loss that can be taken against the actual gain from cash-flow of the property. Additionally, that passive activity loss gets reported on a K-1. Those investors who have K-1 passive activity gains from other business activity are pleasantly surprised to find our paper losses can offset their actual gains and save them taxes in other areas of their portfolio.

We can also front-load our depreciation by using a cost-segregation study. This is called accelerated depreciation, which allows all of the non-permanently affixed items to be depreciated over an even shorter time period (typically 5, 7, or 15 years). I’ve written more on rental property depreciation here.

While depreciation and accelerated depreciation may allow investors to defer taxes on their passive income for many years, it is important to remember that it is not tax elimination. If the property gets sold, the depreciation recapture tax will have to be paid. To avoid that recapture tax, you can employ another tax deferral strategy called a 1031 exchange.

1031 Exchanges – Used When Selling One Investment and Buying Another

Section 1031 of the tax code allows real estate investors to sell a property and use an intermediary to purchase a like-kind property and defer the taxes that would normally be triggered with a sale.

Of course, there are specific rules wrapped around these exchanges, but deferring that tax can potentially allow the investor to grow their wealth faster.

This is why, whenever possible, we prefer to utilize a 1031 exchange when we sell a property.

Refinances – Used to Harvest the Lazy Equity

Of course, as long-term holders of real estate, our preferred liquidity event is a refinance. As equity accumulates in the property through amortization and appreciation, we look to harvest that lazy equity for our investors. That is accomplished through a refinance, which can return a significant portion of the investor’s equity to them.

Refinances do not trigger taxable events and the investor maintains their original equity position in the property. Many investors choose to redeploy that untaxed harvested equity into a new property for increased cash flow.

Legacy Transfer from a Beneficiary Deed – Used When Passing Investments to Heirs

Lastly, long-term holders of multifamily real estate have a significant tax elimination gift from the IRS. This legacy transfer from a beneficiary deed is one of the reasons that so many wealthy people including 90% of the Forbes 400 hold real estate in their portfolio.

The way it works is that both capital gains and depreciation recapture taxes get eliminated upon death. This benefit, provided to the heirs, calls for the basis of the property to get reset to current market value, which eliminates those taxes.

Why Real Estate Tax Benefits Exist

In summary, we’ve seen our multifamily properties provide a wealth of tax benefits to our investors. Those incentives are in the tax code because the government wants investors to provide housing for others. If they are determined to pay me (in the form of lower taxes) for making sound investment decisions then I’m just fine with that. After all, who likes to pay more taxes than they have to?