Correlation and diversification in the multifamily sector

As a private commercial multifamily real estate acquisitions and asset management company, many investors turn to us for portfolio diversification because of our return model and low correlation to the stock market.

When I think about the subject of correlation, I can’t help but harken back to my younger days. Even though college is well in the rearview mirror, I can still remember the discussions of causation and correlation.

Causation tends to be simplistic. It looks at cause-and-effect relationships between two variables and makes absolute connections. Things like:

- It’s raining today so umbrella sales increased.

- At Christmas time more fruitcake sales occur than anytime else during the year.

- Candy sales are higher in February than they are in January because of Valentine’s Day.

While some things do have an absolute cause and effect relationship, most things are not completely black and white. Instead, there are a lot of shades of gray. That’s where correlation steps in.

Correlation measures the degree to which two variables are related and how much they influence each other.

When it comes to investing, correlation is a very important topic. The reason for its importance is that many investors are looking for diversification. Regardless of how you define diversification, it is ultimately the act of owning assets that are as uncorrelated to each other as possible.

Diversification is a risk-mitigation strategy that when applied properly can guard against substantial losses from any one industry or investment

While I risk getting too far in the weeds, I feel obligated to discuss correlation coefficients. The ridiculously long mathematic formula for calculating the correlation coefficient does not need to be memorized to understand this concept.

Basically what you need to know is that the correlation coefficient measures the degree to which two variables are associated and move in relation to one another. The range of values goes from -1.0 to 1.0.

- 1.0 indicates a perfect positive correlation (they move in tandem)

- -1.0 indicates a perfect negative correlation (mirrored movement away from each other)

- 0 means they are uncorrelated (move unrelated to each other)

If I’ve lost you at this point, Investopedia has a great one to two-minute video on the subject that you can.

Therefore, the closer the correlation coefficient is to 0, the more uncorrelated two assets are and the better the diversification. So a correlation coefficient of 0.85 indicates a much higher correlation between two investments than one that is 0.42.

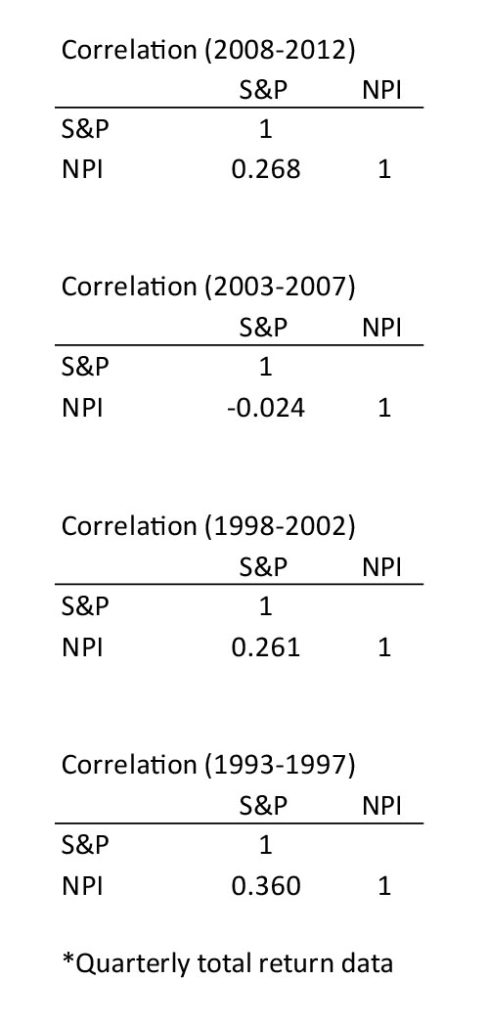

With that said, let’s look at the correlation coefficient between direct commercial real estate (NPI) and the stock market (S&P 500).

Source: University of New Hampshire

As you can see, from 1993 to 2012, direct ownership of commercial real estate has been highly uncorrelated to the stock market. Now keep in mind that the NCREIF Property Index (NPI) factors in several different asset classes of commercial real estate (multifamily, office, retail, hotel, and industrial).

If you wanted to just look at commercial multifamily real estate, the correlation coefficient between it and the S&P 500 over the 30-year period ranging from 1983 to 2012 is an impressive 0.13.

There is no denying the fact that for those who are heavily invested in the stock market, either through individual stocks or mutual funds, commercial multifamily real estate offers an attractive uncorrelated asset class for diversification. Unfortunately, the same cannot be said for REITs.

Going back from 1972 to today, the REIT-stock correlation has fluctuated at a much higher coefficient range of 0.56 – 0.72. It briefly dipped down close to that of direct ownership (NPI), but has since been on a troubling 20-year trend upward. Around 2012 it peaked at an abysmal 0.89. It has subsequently regressed some but remains much more correlated to the stock market than direct ownership of commercial multifamily real estate. Since REITs are nothing more than real estate flavored stock, it isn’t surprising that they act a lot like stock (higher degrees of correlation to the stock market and high volatility).

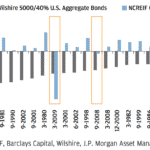

With that said, let’s look at another interesting piece of research.

The above graphic looks at the 20 worst quarters for a 60% stock/40% bond portfolio between 1978 and 2012. Those quarters are all shown in the downward deflected gray bars. The question the researchers wanted to know is how did direct commercial real estate ownership fare during those same quarters?

As it turns out, commercial real estate (blue bars) was up 17 of the 20 quarters that the stock/bond portfolio was down.

The research is clear, commercial multifamily real estate is highly uncorrelated to the stock market. When you combine that fact with the fact that it has low volatility and a history of high average annual returns then it becomes easy to see why so many investors find commercial multifamily real estate an attractive class for diversification.